On Feb. 12, Deschutes County Commissioners had a focused discussion on concerns regarding the state’s recently finalized wildfire hazard map and how residents feel impacted by its designations. Commissioner Patti Adair voiced her opposition to the map at the meeting, citing concerns that the maps are decreasing homeowners’ property values and lowering resale values. This week, some of the region’s state representatives are joining the conversation, calling for an amendment or a full repeal of the map.

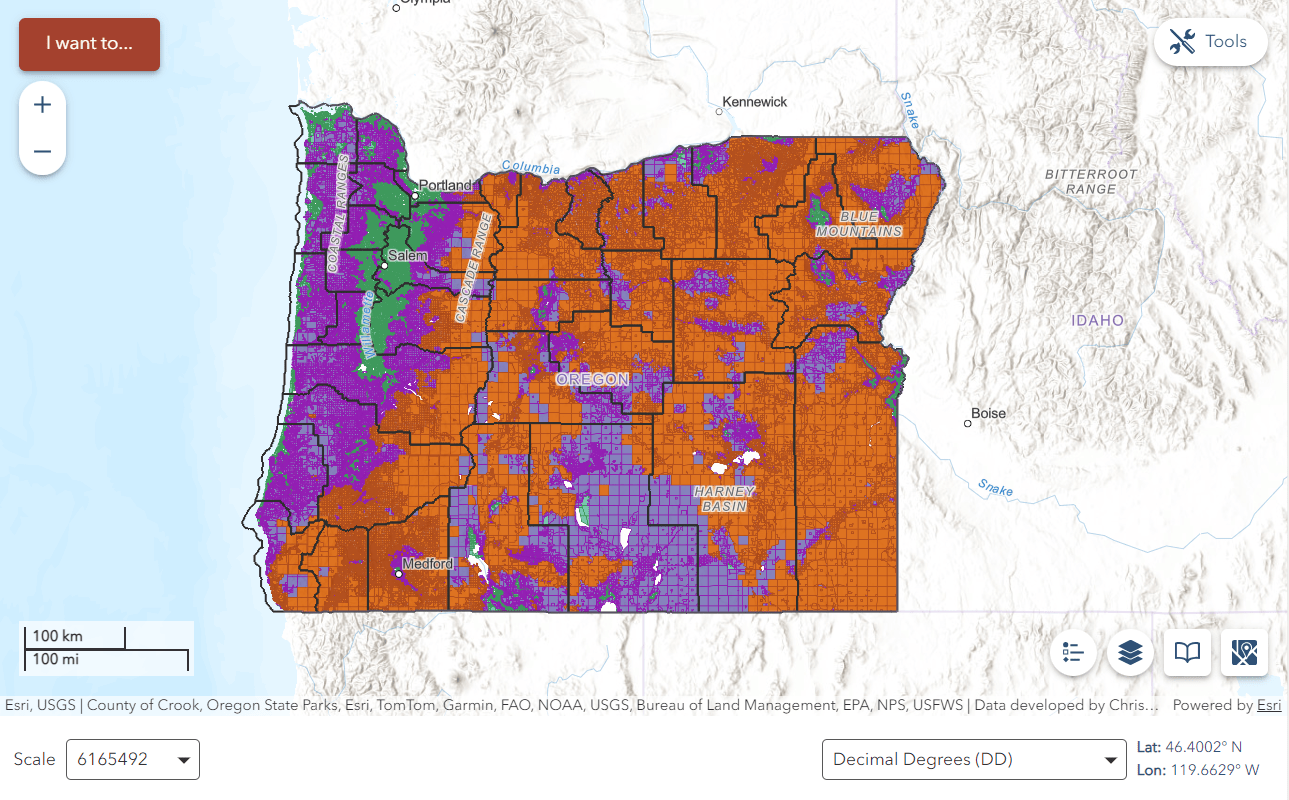

On Jan. 7, the Oregon Department of Forestry released the final version of its statewide wildfire hazard map, designating property tax lots as low-, moderate- or high-hazard zones. The maps are meant to educate residents about their hazard levels and assist in prioritizing mitigation resources and fire adaptions for vulnerable locations. The maps also aim to identify where defensible space and prospective home hardening codes may soon apply.

On Feb. 12, the Deschutes County Board of Commissioners held an impromptu “hearing,” which allowed residents to voice their frustrations about the map.

“The domino effect that possibly got overlooked is costly expense for defensible space with no guarantee of zone reform. [It] unfairly penalized certain property owners with decreased property values and the likelihood of extinct resale value,” said a homeowner in rural Deschutes County at the meeting. “The coincidental non-renewed, cancelation of property fire insurance is a separate issue.”

The initial release of the map in 2022 prompted residents to worry about its role in increasing insurance premiums. However, a bill passed in 2023 makes it illegal for the map to influence insurance companies and their decisions around premiums and coverage. According to the Oregon Division of Financial Regulation, insurers create their own risk models and maps based on their own collected data. Still, Central Oregonians have reported premium increases and coverage retractions.

“I think there’s a lot of misinformation and people are overestimating the impact of these maps,” said Commissioner Phil Chang at the Feb. 12 meeting.

In August, local representatives, officials and insurance representatives met to discuss rising insurance costs. According to Chang, companies are likely charging higher premiums to make up for massive losses from past devastating fires, and to protect themselves moving forward.

Legislators Join the Movement

In early February, Sen. Jeff Golden, D-Ashland, proposed an amendment to SB 762, the bill that created the maps, making the hazard designations for broad areas, rather than individual properties.

On Feb. 20, Sen. Anthony Broadman, who represents Central Oregon, took it a step further, calling for a full repeal of the maps.

“The rigidity of the wildfire maps is not working in communities like mine, and they are distracting from the work we were doing to get ready for the climate and wildfire catastrophe coming this summer and in the future,” Broadman said during a Senate hearing at the Oregon State Capitol.

“I don’t want the maps to distract from the good work we’re doing on fuels reduction, community hardening and preparation for fire season. So, Senators, I encourage a full repeal of the fire maps and let us focus on getting ready for the wildfires that are coming.”

Sen. Golden was supportive of a repeal of the maps, but encouraged legislators to recognize the importance of the work SB 762 has accomplished.

“I really think we have a significant problem with the maps. I think we should repeal them, but we are really going to regret abandoning the other programs in [SB] 762,” he said on Feb. 20.

With significant support from communities to continue wildfire suppression and mitigation work, efforts are also underway at the federal level to offer more resources for Oregonians. This week, U.S. Sen. Ron Wyden helped reintroduce legislation that would make a $60 billion investment in Oregon forests to “lessen wildfire risk, restore watersheds, protect communities and reduce wildfire suppression costs.”

Following these additional calls for action, Adair is hopeful about the potential to repeal the maps.

“I think we’re making serious progress. [Rep.] Emerson Levy and Senator Broadman both came out against it, thank goodness, because it’s incredibly frightening and compounding what it’s done to a lot of people,” Adair told the Source Weekly on Feb. 21. “According to what I’ve heard, the Senate is pretty much on board that the map needs to be repealed. We need to get more support in the House.”

According to Adair, the Board of Deschutes County Commissioners will continue its discussion on the maps at its meeting on Feb. 24, likely deciding if the Board wants to declare its support for the repeal.

This article appears in The Source Weekly February 20, 2025.

MAKE LOCAL JOURNALISM HAPPEN

![]()

Burying your head in the sand would be more effective for wildfire protection than “repealling” the wildfire map. The danger is real and the only protection is to prepare – fuel reduction, infrastructure hardening and emergency procedures. Somehow, even though “efforts are also underway at the federal level to offer more resources for Oregonians”, I have little confidence the current federal administration will oblige.

In order to have any effectiveness in wildfire mitigation the county is going to need to put some sort of pressure on absentee lot owners. Either a tax or some sort of penalty. Otherwise all these efforts and maps and such will be for not.

Even if the map is repealed, it’s out conceptually and insurers will use some version of it to assign risk. Insurers are in the business of covering claims, not giving the homeowners an affordable rate. That’s the harsh truth about insurers, they will increase rates as risk and claims increase which is our reality as homeowners.

Our insurance premiums quadrupled in less than 9 months. Our prior insurance co whom we had been with for 40+ years said “oh sorry, your zip code is classified uninsurable”. We called the state number in the map and were told that “yes” insurers may use “maps” as part of their risk assessment.

The elephant in the room is how will these increasingly high rates affect the new home mortgage market? Will new home buyers seeking affordable homes be able to afford insurance to be eligible for a mortgage?

Resale, ability to stay in one’s long time residence on a fixed income (especially with looming cuts to SS), and the costs of home hardening are the issues in our faces. We choose to live in this environment and will continue efforts for mitigating risk but the eventuality of being uninsured looms on the horizon. How will others fare who do not own their homes outright, can’t afford a mortgage and insurance, and lose marketability when the region is declared uninsurable and/or the pool of insurers diminishes?

Oregon needs an affordable (compared to current rates) state insurance plan, I know, “good luck with that”….

Does repealing the map make these properties less susceptible to wildfire risk? No. In fact, it’s a true representation of what is occurring in our community/ies. It seems like building your house adjacent to a forest comes with an inherent acknowledgement to that risk. Is that true looking back 10+ years, no. Is it clearly true now, yes.

As such, I do think that legislation needs to be passed to protect insurance coverage of the properties purchased in these areas prior to climate changes and official recognition of these risks. (Whether that is through private insurance or a city/state fund. A city/state fund may encourage cities to implement better building guidance in these areas.). But moving forward, it seems reasonable for developers and new buyers to be made aware of these risks and for insurance companies to recognize these areas as higher risk and charge reasonably for newly build homes – much like flood insurance and the disclosure of this risk to homeowners and buyers.

This would also encourage cities to develop more defensible space, rather than extending urban growth boundaries closer and closer to areas at higher risk to wildfire.

As far as property values go, I think this is a tricky discussion. I suppose from a buyer perspective, I would want to be made more aware of the risks of purchasing a home in these often beautiful areas. Just the same as when people look to purchase homes near waterfront. Some waterways are more likely to flood in certain areas and some are not. Acknowledgement of this risk is a protection to future buyers and builders. Should we be continuing to build new homes in high risk areas? Of course, there is a negative impact to current owners, but that’s just like any investment – you don’t know how things will pan out. Friends of ours purchased a house in a quiet neighborhood. Years later, building and parking codes in Bend have changed and now there is a proposal to put a 100+ unit dorm-like apartment building with limited off-street parking and potential commercial space on what was previously a single family lot. If built, this will drastically change the neighborhood – impacting traffic and livability in the area, and likely affecting home values as streets become more crowded with parked cars and increased road noise. Of course this is disappointing from a personal investment standpoint, but I imagine people living on large lots adjacent to forest would argue that we need to acknowledge the need for more housing. We can’t have our cake and eat it too.

We can reduce wildfire risk to homes by building in more defensible space. We can make our city more livable by investing in infrastructure to support changes in building and development codes first. We need the city to to help with implementing guidance, code, and regulation that specifically looks at our city’s unique needs instead of hiding a map behind closed doors.

Obviously this is a very nuanced issue and I will not pretend that I have all the information and knowledge of all the challenges we face to ensure equity is preserved and protected as we grow as a community. However, these issues are only going to become more relevant as we continue to elect people into government who prioritize short term solutions and gains over long-term planning and investment.